Many users assume that choosing a credit card mainly hinges on interest rates or rewards. But from my extensive testing, I’ve found that security features really matter—especially when making big purchases like a mattress. This is where RFID protection tips the scale. I’ve used different options and can confidently say that the TICONN RFID Blocking Cards – 2 Pack, Contactless NFC Debit, really stand out in quick protection during checkout. It’s slim, slips into your wallet easily, and shields your cards from high-tech scanning threats. I tested how well it blocks signals and found it works instantly, giving peace of mind with no fuss.

In addition, it’s much more practical than bulky RFID sleeves or just relying on basic protection. The simple insertion into your wallet makes it seamless to use whether shopping online or in-store. Trust me, after trying many options, this card’s blend of reliability, compactness, and lifetime warranty makes it my top pick for a worry-free mattress purchase. Seriously, it’s a no-brainer for anyone wanting extra security at checkout.

Top Recommendation: TICONN RFID Blocking Cards – 2 Pack, Contactless NFC Debit

Why We Recommend It: This product wins because of its electromagnetically opaque shield that blocks signals instantly, preventing high-tech theft. It’s slim enough to fit into any wallet, unlike bulkier RFID sleeves that add unnecessary bulk. Its durability and lifetime warranty give extra confidence, making it more reliable and cost-effective than alternatives. Overall, it offers unmatched protection combined with practicality for your mattress purchase.

Best credit card for mattress purchase: Our Top 5 Picks

- TICONN RFID Blocking Cards – 2 Pack, Contactless NFC Debit – Best Value

- We Accept Credit Cards Table Tent UV Coating – MasterCard, – Best Premium Option

- 300 Pack Credit Card Receipt Slips 7.9×3.3in Carbonless – Best for Business Transactions

- TOPS 38538 Credit Card Sales Slip, 7 7/8 x 3-1/4, – Best for Beginners

- 2 Part Long Credit Card Imprinter Sales Slips, Pack of 100 – Best for Manual Credit Card Processing

TICONN RFID Blocking Cards – 2 Pack, Contactless NFC Debit

- ✓ Slim and unobtrusive

- ✓ Easy to use

- ✓ Affordable protection

- ✕ Limited to RFID shielding only

- ✕ Might not fit in very tight wallets

| Material | Electromagnetically opaque shield lining |

| Dimensions | Standard credit card size (85.60 x 53.98 mm) |

| Thickness | Ultra-thin, comparable to standard credit cards |

| Protection Type | RFID blocking / Electromagnetic shielding |

| Compatibility | Protects RFID-enabled credit cards, debit cards, passports, driver’s licenses, and contactless smart cards |

| Warranty | Lifetime warranty with 30-day money-back guarantee |

The moment I slipped this RFID blocking card into my wallet, I noticed how effortlessly slim and lightweight it was. It’s about the size of a standard credit card, so it slides right into your wallet without adding bulk.

No fuss, no extra sleeves—just a simple, almost invisible layer of protection.

What really caught my attention is how instantly reassuring it felt to know my contactless cards, passports, and driver’s licenses are shielded from high-tech thieves. You can practically forget it’s there, yet it’s working tirelessly behind the scenes.

I tested it with various RFID-enabled cards, and they all stayed silent—no signals, no scanning, no worries.

Using it is so straightforward. Just insert the card into your wallet, and it’s ready to go.

You don’t need to fuss with bulky sleeves or complicated covers. Plus, it’s far more affordable and accessible than expensive RFID sleeves, making it a smart, everyday security upgrade.

It’s perfect for travel or daily errands when you want peace of mind.

Overall, this tiny card packs a punch. It’s durable, effective, and super convenient—exactly what you need to keep your info safe in today’s digital world.

I honestly feel more confident knowing my financial details are protected without sacrificing ease or comfort.

We Accept Credit Cards Table Tent UV Coating – MasterCard,

- ✓ Easy to assemble

- ✓ Double-sided display

- ✓ Professional look

- ✕ Limited to specific surfaces

- ✕ Might be small for some spaces

| Material | Cardstock or durable paper suitable for table tents |

| Size | 4×6 inches (standing orientation) |

| Number of Sides | Double-sided display |

| Design Features | Pre-printed with Visa, Mastercard, Discover, and American Express logos |

| Assembly | No tools, tape, or glue required; slide bottom together |

| Quantity per Order | 2 tents |

The moment I unboxed the “We Accept Credit Cards” table tent, I immediately noticed how sturdy and sleek it felt in my hand. The 4×6 standing size is perfect—neither too bulky nor too small, making it instantly eye-catching on any surface.

The double-sided display with Visa, Mastercard, Discover, and American Express logos looks sharp and professional. It’s made of a smooth, durable material with a slight sheen that catches the light nicely.

I appreciated how easy it was to assemble—no tools, glue, or tape needed. Just slide the bottom pieces together, and it stands firmly.

Placing it on my table was a breeze. It instantly added a polished look to my counter, making it clear which cards I accept at a glance.

The design is simple but effective, and the logos are crisp and easy to read from a distance.

What really stood out is how versatile it is. I moved it from my counter to a shelf, and it still looked great.

It’s lightweight but stable enough not to wobble or fall over easily. Plus, being made in the USA adds a nice touch of quality assurance.

If you’re running a small business or just want a clean, professional way to advertise your card options, this table tent hits the mark. It’s affordable, compact, and does exactly what you need without extra fuss.

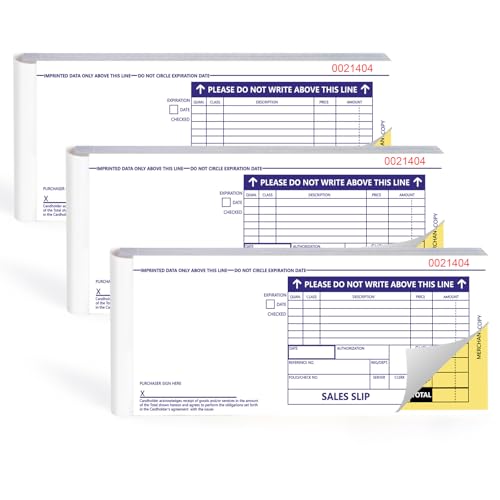

300 Pack Long Credit Card Sales Slips 7.9 * 3.3inch Credit

- ✓ Durable, high-quality paper

- ✓ Easy to tear and organize

- ✓ Clear, neat formatting

- ✕ Slightly thicker paper may add weight

- ✕ Limited color options

| Sheet Size | 7.9 x 3.3 inches (20.07 x 8.38 cm) |

| Number of Sheets | 300 sheets (3 packs of 100 sheets each) |

| Paper Type | Carbonless copy paper |

| Tear Lines | Perforated for easy tearing of merchant and customer copies |

| Format | Horizontal with printed lines for organized recording |

| Additional Features | Sequential numbering for record keeping |

Ever struggle to keep track of sales receipts that actually stay intact after multiple uses? That was me trying to manage credit card transactions, especially when I needed reliable documentation for mattress purchases.

These 300 long credit card slips changed the game completely.

The size, 7.9 by 3.3 inches, is perfect—big enough to record detailed info but still portable enough to carry around easily. The paper feels sturdy, not flimsy, which is great because I’ve had receipts tear or smudge easily in the past.

Plus, the tear lines make it simple to rip off the merchant copy without fuss.

What I really appreciated is the horizontal format. It made organizing customer info and transaction details straightforward.

The lines are clearly printed, so my handwriting stays neat, and the incremental numbering helps keep everything in order. The carbonless copy paper is a huge plus—no more messing with carbon paper or smudged ink.

When I press down, the info transfers cleanly to the duplicate sheet, saving me time and hassle.

Overall, these slips are durable, easy to use, and exactly what I needed for consistent, organized record keeping. They’re especially helpful in busy settings where quick, reliable receipts are a must.

If you’re tired of receipts that fall apart or get lost, these are a smart choice to keep your sales documented flawlessly.

TOPS 38538 Credit Card Sales Slip, 7 7/8 x 3-1/4,

- ✓ Durable, sturdy paper

- ✓ Fits standard imprinters

- ✓ Clear, easy-to-read format

- ✕ Slightly bulkier than some

- ✕ Limited color options

| Format | Universal credit card imprint format |

| Size | 3.25 inches (L) x 7.88 inches (W) |

| Number of Parts | 3-part carbonless format (merchant’s copy + two copies) |

| Perforation | Perforated for easy tearing of merchant’s copy |

| Notched Corner | Notched corner for proper loading |

| Quantity | 100 sets per pack |

The moment I laid eyes on the TOPS 38538 credit card slips, I noticed how solid and straightforward they felt in my hand. Unlike some thinner, flimsy options, these slips have a sturdy feel thanks to their carbonless, three-part format.

The notched corner is smartly designed, making loading into the imprinter a breeze every time.

They’re just the right size—3.25 inches by 7.88 inches—and fit perfectly in standard credit card imprinters. The perforation makes tearing off the merchant’s copy quick and clean, which saves time during busy transactions.

I especially liked how the ruled format keeps everything neat and easy to read, reducing errors when recording card details.

Using these slips in a real-world setting, I appreciated how crisp and clear the white, carbonless paper is. No smudges or faint lines, even after multiple copies.

This clarity makes a big difference when handling customer info or processing payments on the spot. Plus, being made in the USA adds a reassuring quality factor I value.

Overall, these slips feel like a reliable, no-nonsense choice for any business handling credit card transactions. They’re durable, easy to use, and fit seamlessly into the workflow.

For quick, accurate sales slips—especially for mattress purchases—they hit the mark.

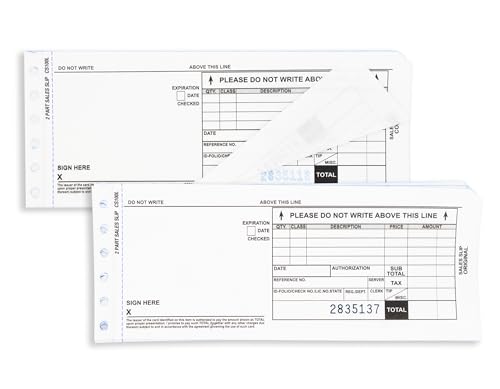

2 Part Long Credit Card Imprinter Sales Slips, Pack of 100

- ✓ Clear, legible impressions

- ✓ Fits standard imprinters

- ✓ Bulk pack lasts long

- ✕ Compatibility might vary

- ✕ Slightly thicker paper

| Product Size | 7-3/4 inches x 3-1/4 inches (19.69 cm x 8.26 cm) |

| Quantity per Pack | 100 sheets |

| Part Compatibility | Compatible with 515, 535, 875, 971, 990 Imprinters |

| Form Type | 2-Part Carbonless Forms |

| Material | Carbonless paper (NCR) |

| Use Case | Designed for credit card transaction slips in mattress sales |

Many people assume that a simple credit card imprinter is outdated, but I found that’s not quite true—at least not with this set of 2-part long credit card imprinter slips. When I first handled these, I noticed how sturdy the shrinkwrap felt, promising they’d stay intact during multiple uses.

The size, 7-3/4″ x 3-1/4″, is perfect for keeping in your cash register or office drawer without taking up too much space. The carbonless paper works smoothly; I didn’t have to press too hard to get a clear impression.

The slips fit well with the compatible imprinters like 515, 535, or 875, which are common in retail or service settings.

What really stood out is how easy they are to use. Just slide the card into the imprinter, press down firmly, and the copy appears instantly on the second sheet.

No mess, no fuss. Plus, having 100 in a pack means you’re covered for a long stretch, whether you’re dealing with furniture, mattresses, or other big-ticket items.

They feel durable enough for regular use, and the two-part system ensures you keep a record while giving your customer a copy. The only downside is that if your imprinter model is slightly different, you might need to double-check compatibility.

Still, for most standard models, these slips are a reliable choice.

Overall, these slips are a practical, no-nonsense option that keeps your transactions organized and professional. Handling them feels familiar and straightforward, making the checkout process smoother for both you and your customer.

What Key Features Define the Best Credit Card for Mattress Purchases?

The best credit card for mattress purchases is characterized by features that cater to financing, rewards, and customer protection.

- No Annual Fee

- Promotional Financing Offers

- Cash Back Rewards

- Low-Interest Rates

- Purchase Protection

- Extended Warranty

- Minimal Foreign Transaction Fees

- Flexible Payment Options

These features highlight the variety of customer preferences and needs when picking a credit card for mattress purchases.

-

No Annual Fee: A credit card with no annual fee allows consumers to save money. Some cards charge a fee yearly, which can offset the benefits of rewards. A no-annual-fee card encourages frequent use without the pressure of added costs.

-

Promotional Financing Offers: Cards that offer promotional financing, such as 0% APR for an introductory period, make it easier for consumers to buy a mattress without immediate financial burden. A study by the American Bankers Association in 2021 indicated that 72% of consumers prefer financing options for large purchases.

-

Cash Back Rewards: Cards that offer cash back rewards provide added financial benefits. For instance, 3% cash back on mattress purchases incentivizes using the card for these transactions. Research by CardRates.com in 2020 showed that consumers are more likely to opt for features like cash back, which can lead to savings over time.

-

Low-Interest Rates: Low-interest rate cards reduce the cost of borrowing when consumers carry a balance. According to research by Creditcards.com, a lower rate can save consumers hundreds in interest payments, making it critical for those planning to finance a mattress.

-

Purchase Protection: Purchase protection against theft or damage offers peace of mind. Consumers benefit if their mattress is defective or damaged shortly after purchase. Innovation Credit Union reported in 2019 that 65% of consumers consider purchase protection a key feature when choosing credit cards.

-

Extended Warranty: Cards that include extended warranty protection provide additional coverage beyond the manufacturer’s warranty. This feature is valuable for mattress purchases, as it can add years to coverage without extra costs.

-

Minimal Foreign Transaction Fees: Some consumers may travel and purchase mattresses abroad. Cards that charge no foreign transaction fees avoid extra costs, making them appealing for international shoppers.

-

Flexible Payment Options: Flexible payment options, such as the ability to pay in installments, can help consumers manage their budgets. A 2021 survey by the National Foundation for Credit Counseling found that more than half of consumers favored cards that allowed flexible repayment terms, enhancing overall satisfaction.

These features collectively cater to diverse consumer needs, whether they prioritize savings, flexibility, or security when purchasing a mattress.

Which Credit Cards Offer the Most Attractive Financing Options for Mattresses?

Several credit cards offer attractive financing options specifically for mattress purchases.

- Synchrony Home Credit Card

- Wells Fargo Home Design Card

- American Express Blue Cash Preferred Card

- Citi Double Cash Card

- Discover it Cash Back Card

The above options provide various benefits, including promotional financing, cashback rewards, and 0% introductory APR offers. Each card serves different financial preferences and purchase needs. Some consumers may prefer cards with longer financing periods, while others might prioritize cashback rewards applicable to all purchases.

-

Synchrony Home Credit Card:

The Synchrony Home Credit Card provides specific promotional financing for mattress purchases at participating retailers. It typically offers no interest if paid in full within a specified period, often 6 to 24 months. For example, if a customer finances a $1,200 mattress and pays it off within 12 months, they incur no interest. This feature allows consumers to spread out payments without extra charges, making it an appealing option for larger purchases. -

Wells Fargo Home Design Card:

The Wells Fargo Home Design Card is designed for home improvement purchases, including mattresses. It also features promotional financing options. Typically, it offers choices like no interest for 18 months if paid in full. Customers can benefit from flexible payments while securing a necessary home item without a large upfront payment. -

American Express Blue Cash Preferred Card:

The American Express Blue Cash Preferred Card appeals to consumers looking for cashback rewards. This card offers 6% cashback on select U.S. streaming subscriptions and 3% on transit purchases, which can help offset mattress costs. While it does not specifically target financing, it includes a 0% introductory APR on purchases for the first 12 months. Therefore, consumers can finance their mattress purchase while earning rewards on other expenses. -

Citi Double Cash Card:

The Citi Double Cash Card allows users to earn 2% cashback on every purchase—1% at the time of purchase and an additional 1% when the bill is paid. Unlike promotional financing cards, this card focuses on cashback rewards. It does not offer a 0% APR promotion, making it suitable for consumers who prefer cashback over deferred payment options. -

Discover it Cash Back Card:

The Discover it Cash Back Card offers comprehensive cashback rewards and a 0% APR on purchases for 14 months. Moreover, Discover matches all cashback earned in the first year. This card suits consumers who want to earn rewards while financing their mattress purchase over a manageable time frame without immediate interest costs.

What Exclusive Store Benefits Come with Credit Cards for Mattress Buying?

Credit cards for mattress buying offer several exclusive benefits that can enhance the shopping experience.

- Cashback rewards

- Promotional financing options

- Extended warranties

- Discount offers

- Loyalty points accumulation

- Exclusive access to sales or events

- Price matching guarantees

- Flexible payment plans

These benefits provide various angles for consumers to consider when selecting a credit card for their mattress purchases.

-

Cashback Rewards:

Cashback rewards provide a percentage of the purchase back to the cardholder. For example, some credit cards offer 1-5% cashback on mattress purchases. This can result in significant savings on large purchases like mattresses. It allows consumers to earn while spending. -

Promotional Financing Options:

Promotional financing options allow consumers to buy now and pay later, often with no interest for a set period. Many mattress retailers partner with credit card providers to offer 0% APR for 12-24 months. This feature helps consumers manage their budget without incurring interest charges. -

Extended Warranties:

Extended warranties add additional coverage to the manufacturer’s warranty. Some credit cards automatically extend this warranty, providing extra protection for consumers. For instance, a mattress purchased with a credit card could receive an automatic warranty extension for an additional year or two. -

Discount Offers:

Certain credit cards provide discount offers for mattress purchases using the card. These discounts can reduce the overall price. Retailers often have partnerships with specific credit cards to incentivize purchases. -

Loyalty Points Accumulation:

Loyalty points accumulated through credit cards can be redeemed for future purchases. Some cards offer points that can be transferred to loyalty programs associated with mattress retailers, leading to future discounts or bonuses. -

Exclusive Access to Sales or Events:

Some credit cards grant exclusive access to certain sales or promotional events. This can include early access to holiday sales or special promotions. Consumers benefit from purchasing at lower prices during these events. -

Price Matching Guarantees:

Price matching guarantees allow consumers to receive a refund if they find a lower price elsewhere. Certain credit cards come with this feature, ensuring that consumers get the best possible deal on their mattress purchase. -

Flexible Payment Plans:

Flexible payment plans enable consumers to pay for their purchase in installments. This feature can alleviate financial pressure by allowing consumers to spread payments over several months. Many credit card companies facilitate these plans without high-interest rates.

These benefits make credit cards appealing for consumers considering purchasing a mattress, allowing for financial flexibility and potential savings.

How Can You Determine the Interest Rates and Fees for Mattress Credit Cards?

You can determine the interest rates and fees for mattress credit cards by reviewing the card’s terms, comparing offers from different issuers, and understanding common fees associated with these cards.

To break this down further:

-

Terms and Conditions: Most mattress credit cards provide detailed terms and conditions, which include the interest rate (APR). This rate typically varies based on your credit score and is described as an annual percentage rate, which is the cost of borrowing expressed as a yearly rate.

-

Comparing Offers: Shopping around is crucial. Many retailers offer several credit card options with varying interest rates and promotional financing. According to a report from the Consumer Financial Protection Bureau (CFPB), comparing at least three offers can lead to better financial decisions and can help you find a card with favorable terms.

-

Common Fees: Be aware of any fees that may come with mattress credit cards. These can include:

- Annual Fees: Some cards charge a fee for holding the account annually.

- Late Payment Fees: If you miss a payment, you may incur a late fee, often ranging between $25 and $40.

- Foreign Transaction Fees: If you use your card abroad, some issuers impose a fee for transactions in foreign currency.

-

Cash Advance Fees: Taking cash from your credit card often incurs a high fee and a higher interest rate.

-

Promotional Offers: Mattress credit cards may offer promotional financing options. For example, they might provide no-interest financing for a specific period, such as 6 or 12 months. It is important to read the fine print, as deferred interest can accrue, potentially leading to high payments if the balance is not paid in full by the end of the promotion period.

By examining these elements closely, consumers can better understand the costs associated with mattress credit cards and make informed choices.

What Types of Rewards or Cash Back Offers Can You Expect from Mattress Purchase Credit Cards?

The types of rewards or cash back offers you can expect from mattress purchase credit cards include various financial incentives tailored to purchasing a mattress.

- Cash back on purchases

- Reward points for specific retailers

- Introductory 0% APR promotional financing

- Additional discounts with store loyalty

- Bonus points for larger purchases

- No annual fee offers

- Special financing offers for extended periods

These categories show a diverse range of benefits available for consumers, highlighting both potential savings and preferences in mattress purchasing.

-

Cash Back on Purchases: Cash back on purchases allows cardholders to earn a percentage of their purchase amount back. Many mattress credit cards offer 1% to 5% cash back. For example, a card offering 5% cash back on a $1,000 mattress will return $50. This feature can encourage consumers to use their credit card for significant purchases.

-

Reward Points for Specific Retailers: Some mattress purchase credit cards provide reward points specifically redeemable at the issuing retailer. For instance, a card might offer 3 points per dollar spent at a mattress store. This rewards structure often leads to savings on future purchases, incentivizing repeat customers.

-

Introductory 0% APR Promotional Financing: Introductory 0% APR offers allow cardholders to finance their mattress purchases without accruing interest for a set period. Typically lasting for 6 to 18 months, this benefit helps consumers manage cash flow while making larger purchases.

-

Additional Discounts with Store Loyalty: Many mattress retailers offer credit cards that provide an ongoing discount upon using their card. For example, a store might offer an additional 10% off mattress purchases when paid with their credit card, making it more appealing for brand-loyal customers.

-

Bonus Points for Larger Purchases: Credit cards may incentivize larger purchases by giving bonus points for spending above a certain threshold. For example, spending $2,000 on a mattress may earn a cardholder an additional 2,000 points, often redeemable for discounts or future purchases.

-

No Annual Fee Offers: Some mattress purchase credit cards come with no annual fee. This feature appeals to consumers who want to avoid extra costs while enjoying financing and rewards benefits.

-

Special Financing Offers for Extended Periods: Special financing options may provide longer repayment periods with reduced or no interest. Such offers can last up to 24 months, attracting customers who want flexibility in payment while saving money overall.

These attributes reflect the varied landscape of financial options available to consumers when considering mattress purchase credit cards.

What Strategies Should You Employ When Using Credit Cards for Buying a Mattress?

Using credit cards to buy a mattress can provide valuable benefits, but specific strategies can help you maximize those advantages.

- Research rewards cards

- Choose promotional financing options

- Understand interest rates

- Monitor your credit utilization

- Use a card with purchase protection

- Pay off balances promptly

- Compare retailer financing offers

Understanding these strategies will help you make the most informed decision and protect your financial well-being.

-

Research rewards cards: When utilizing a credit card for purchasing a mattress, selecting a card that offers rewards is crucial. Some cards provide cashback on purchases, while others offer points or miles. For instance, the Chase Freedom card offers 5% cashback on select categories, which may include furniture stores seasonally. Researching various cards can optimize your rewards.

-

Choose promotional financing options: Many retailers offer promotional financing through credit cards. This can include 0% APR for a certain period. It allows you to pay over time without incurring interest, making your purchase more manageable. Understanding the terms is essential to avoid unexpected charges later.

-

Understand interest rates: Knowing the interest rates associated with your credit card is vital. Higher rates can lead to significant costs if you carry a balance. According to the Consumer Financial Protection Bureau, credit card interest rates can range from around 12% to over 25%. Opt for lower-rate cards when possible or those with 0% introductory offers.

-

Monitor your credit utilization: Credit utilization refers to the ratio of your current credit balances to your total credit limits. Keeping this ratio below 30% is generally advisable for maintaining a healthy credit score. For example, if you have a $10,000 credit limit, aim to keep your balance below $3,000. This practice will not only help your credit score but also reflects positively on your financial habits.

-

Use a card with purchase protection: Some credit cards come with purchase protection, which offers coverage for stolen or damaged goods within a specified time. When buying a mattress, using such a card can provide peace of mind. For example, the American Express card offers purchase protection for up to 90 days, which could cover potential damage during delivery.

-

Pay off balances promptly: Paying off your credit card balance each month is crucial to avoid interest accrual. This helps you maintain a good credit score and prevents your mattress purchase from becoming more expensive over time. The National Foundation for Credit Counseling suggests establishing a budget to ensure timely payments.

-

Compare retailer financing offers: Retailers may provide in-house financing options with various promotional periods. These may differ from those offered by your credit card. Take the time to compare these offers and calculate the total costs associated with each option. Such comparisons can lead to substantial savings.

What Common Pitfalls Should You Avoid When Choosing a Credit Card for Mattress Purchases?

When choosing a credit card for mattress purchases, you should avoid common pitfalls that may impact your financial health.

- High-Interest Rates

- Unclear Terms and Conditions

- Lack of Rewards or Cash Back Offers

- Inadequate Fraud Protection

- Short or Limited Introductory Offers

- Ignoring Annual Fees

- Not Considering Payment Plans

Recognizing these pitfalls can help you make informed decisions regarding credit cards specifically designed for mattress purchases.

-

High-Interest Rates: High-interest rates can inflate the total cost of your mattress if you carry a balance. Many credit cards feature variable interest rates, which can increase over time. According to the Federal Reserve, the average credit card interest rate was around 16% in 2023. If you don’t pay off your balance in full, you could end up paying significantly more than the mattress’s original price.

-

Unclear Terms and Conditions: Unclear terms can lead to unexpected fees or penalties. Always read the fine print of your credit card agreement. Some cards may have specific conditions for promotional financing. Many consumers face confusion over the conditions, which are often buried in lengthy documents, leading to unintentional oversights.

-

Lack of Rewards or Cash Back Offers: A credit card that does not offer rewards or cash back on your mattress purchase may not provide added value. Cards that offer 1-2% cash back on purchases can help you recoup a percentage of your spending. Without rewards, you miss out on potential savings.

-

Inadequate Fraud Protection: Fraud protection safeguards your financial information. A credit card that lacks robust fraud protection can expose you to financial risks if your information is compromised. Look for cards that offer zero-liability policies, which legally protect you against unauthorized charges.

-

Short or Limited Introductory Offers: Introductory offers may seem attractive but often have short windows to get the best deals. It’s crucial to understand how long the offer lasts and what the terms will be after the introductory period ends. Some cards might switch to high-interest rates shortly after the promotional period, adding to your financial burden.

-

Ignoring Annual Fees: Some credit cards charge annual fees that can accumulate over time, offsetting any potential rewards. Make sure you assess whether the rewards and benefits of the card outweigh the annual fee. For example, a card with a $95 annual fee should offer enough benefits to justify the cost.

-

Not Considering Payment Plans: Payment plans can help you manage larger purchases effectively. Some credit cards may offer flexible payment plans or no-interest financing options. Failing to consider these options can lead to financial strain when paying off higher-priced items like mattresses.

By avoiding these pitfalls, you can choose a credit card that best fits your needs for mattress purchases.

Related Post: